The attempt by Sunway Berhad to “lock in” control of IJM Corporation Berhad through a voluntary Mandatory General Offer (MGO) has ultimately reached a dead end after failing to secure the critical majority threshold. The offer officially lapsed on 6 April 2026, having garnered only approximately 33.43% of voting rights—well short of the minimum 50% required to gain control.

This failure cannot be dismissed as merely technical. Rather, it reflects a broader strategic miscalculation in assessing the true sentiment of IJM’s shareholders. What appeared to be a determined push led by Jeffrey Cheah has instead backfired, exposing what critics describe as an overconfident and misjudged attempt to force through a high-stakes corporate move.

Although the acquisition resolution received near-unanimous approval from Sunway shareholders at its Extraordinary General Meeting (EGM) on 26 March, the reality on the ground told a different story. IJM shareholders remained unmoved. Their rejection, delivered quietly but decisively, sent a strong signal that the offer failed to reflect the true strength and long-term value of IJM’s assets.

As the deadline for the MGO approached, a critical development unfolded. Permodalan Nasional Berhad (PNB) and the Employees Provident Fund (EPF / KWSP), both among the largest institutional shareholders in IJM, unexpectedly withdrew from the process and chose not to dispose of their shares—effectively dealing a decisive blow to the takeover effort.

Market Narrative Under Scrutiny

From the outset, questions had been raised over the foundation of the offer—ranging from valuation concerns to a broader market narrative that appeared to weaken perceptions of IJM. The situation was further complicated by developments involving IJM Chairman Krishnan Tan, whose remand and scrutiny by tax authorities cast a shadow over the company.

Reports of bank accounts under investigation—amounting to nearly RM100 million—alongside revelations involving his investment advisor Seow Lun Hoo, who was linked to accounts totalling approximately RM2.5 billion, added further pressure to the narrative surrounding IJM at a critical time.

IJM is far from a marginal entity. It holds strategic national assets, including toll highways, long-term concessions and port operations that directly contribute to the country’s economic framework. As such, any attempt to acquire the company at a valuation perceived as unconvincing inevitably raises a fundamental question—who stands to benefit from such a transaction, and what interests are truly at play behind it?

Controversial Developments and Market Narrative

The situation worsened following the high-profile scrutiny involving IJM Chairman Krishnan Tan, whose financial dealings reportedly came under investigation by tax authorities.

The exposure of alleged bank accounts—including figures nearing RM100 million and links to financial advisors with accounts reaching RM2.5 billion—has further damaged market confidence.

This raises a critical question: Was the market narrative deliberately shaped to weaken IJM’s valuation ahead of the takeover attempt?

Backdoor Engagements with GLICs

Statements by Sunway Berhad claiming that early discussions had taken placein relation to the takeover attempt have sparked significant controversy. IJM Corporation Berhad has firmly denied that any formal negotiations occurred prior to 12 January 2026, describing Sunway’s assertions as misleading.

According to IJM, any communication before that date was limited to a request for a meeting and did not constitute formal deal negotiations. This distinction is critical, as it directly challenges the narrative presented by Sunway and raises concerns about the accuracy of disclosures made during the process.

More troubling, however, is the possibility that preliminary discussions may have taken place with institutional shareholders—particularly Government-Linked Investment Companies (GLICs)—without the knowledge of IJM’s board of directors and management. Such a scenario suggests that key elements of the takeover may have been orchestrated outside formal governance structures, pointing to the involvement of larger and more influential parties behind the scenes.

IJM has indicated that if such engagements did occur, they were conducted beyond the oversight of its board and management, thereby raising serious questions about corporate governance, transparency and the integrity of the takeover process.

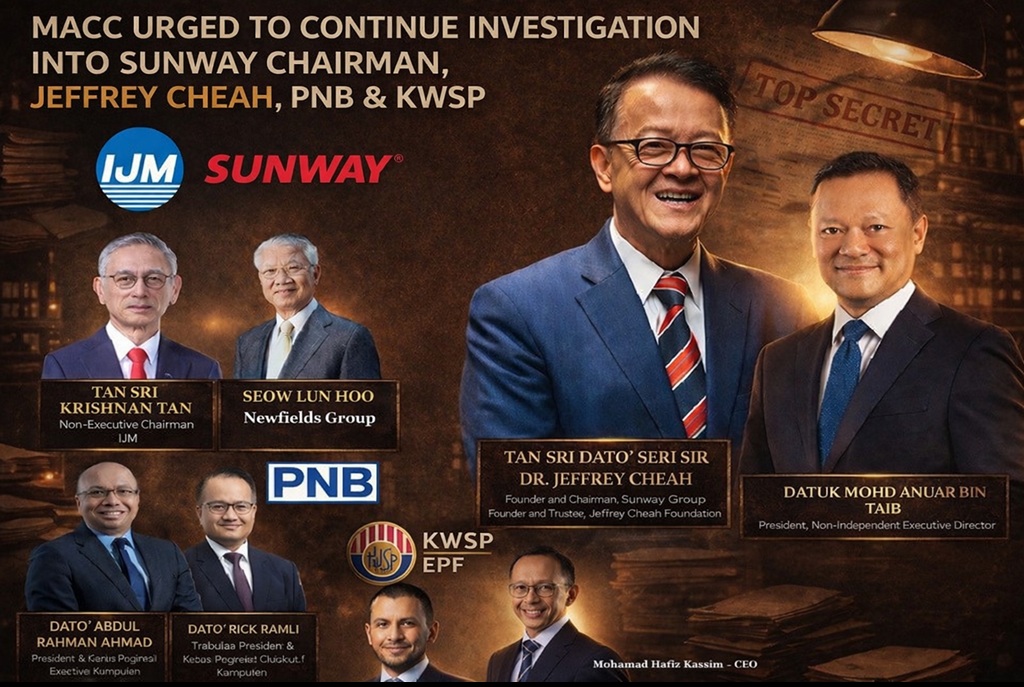

This leads to a pressing question: who was the early negotiator operating behind IJM? Speculation has emerged around Ahmad Fuad Md Ali, a member of PMAC at Menara KLCC, who has been widely discussed on social media in connection with the matter. He is alleged to have leveraged his position in relation to the IJM share sale to influence or persuade the boards of Permodalan Nasional Berhad (PNB) and the Employees Provident Fund (EPF / KWSP).

It is increasingly difficult to accept that such a complex and high-level operation could have been executed by Jeffrey Cheah alone, without the involvement of powerful actors and major shareholders within IJM.

Who Is Behind This Strategic Play?

On Sunway’s side, Anuar Taib, the President of Sunway Berhad, has emerged as a central figure in the execution of the strategy. Known for his controversial past associations with Petronas and Sapura Energy Berhad, Anuar is now widely regarded as a close confidant of Jeffrey Cheah.

He is believed to have been tasked by Jeffrey Cheah to leverage his influence and network in an effort to secure control of IJM Corporation Berhad. His role, positioned at the intersection of corporate strategy and institutional engagement, has drawn increasing scrutiny as questions continue to mount over how the takeover attempt was orchestrated behind the scenes.

He was required to engage and negotiate with two major government-linked investment institutions, as the largest shareholders of IJM—Permodalan Nasional Berhad (PNB) and the Employees Provident Fund (EPF / KWSP). He came close to securing their alignment, but ultimately fell short.

This raises a critical question: who were the key figures within Permodalan Nasional Berhad?

- YM Raja Tan Sri Dato’ Seri Arshad Raja Tun Uda — Chairman of PNB

- Dato’ Abdul Rahman Ahmad — President and Group Chief Executive Officer

- Datuk Rick Ramli — Deputy President and Group Chief Executive Officer

Reports indicate that Datuk Rick Ramli played a significant role within PNB, acting as a key link connecting the institution’s Chairman and CEO to Tan Sri Dr Jeffrey Cheah during the course of the transaction.

For the Employees Provident Fund (EPF / KWSP), two key figures have been identified:

- Ahmad Zulqarnain Onn — Chief Executive Officer

- Mohamad Hafiz Kassim — Chief Investment Officer

Both Ahmad Zulqarnain and Mohamad Hafiz Kassim are understood to have played central roles in preparing the investment framework that would have enabled Sunway Berhad to acquire EPF’s stake in IJM Corporation Berhad.

However, at the final stage, EPF is believed to have withdrawn from the transaction amid mounting public exposure and a wave of objections, effectively halting what had appeared to be a near-complete alignment.

Proxy to the IJM Chairman

Another figure drawing attention is Seow Lun Hoo the founder of investment firm Newfields Group. He is understood to have served as an investment advisor to IJM Chairman Krishnan Tan and is currently under investigation by the Malaysian Anti-Corruption Commission (MACC) in connection with an alleged RM2.5 billion money laundering scandal.

According to sources, prior to his retirement, Krishnan Tan is believed to have coordinated with Jeffrey Cheah in efforts to facilitate the sale of IJM Corporation Berhad to Sunway Berhad. The alleged motive behind these arrangements, as suggested by sources, was financial gain.

Allegations of Corruption Involving Jeffrey Cheah

The individuals named are alleged not to have been involved by coincidence, but rather as part of a coordinated network believed to have been promised substantial financial rewards by Jeffrey Cheah to facilitate the takeover process. Within this alleged structure, Anuar Taib is said to have played a proxy role, while informal approvals—or “green lights”—from institutional actors such as Permodalan Nasional Berhad (PNB) have been linked to figures including Abdul Rahman Ahmad and Rick Ramli.

What unfolded is alleged to be far from a routine corporate transaction. Instead, it is described as a high-profile deal potentially involving commissions amounting to millions of ringgit. More troubling is the suggestion of a corporate cartel willing to exploit positions within public investment institutions to influence the transfer of strategic national assets for private gain. This is no longer merely a matter of business—it raises fundamental concerns about the breach of public trust.

Viewed through this lens, the attempted acquisition of IJM Corporation Berhad by Sunway Berhad appears less like a conventional corporate move and more like a calculated operation involving influential individuals and internal networks. Allegations of proxy roles and informal approvals from key parties raise serious questions about the integrity of the process—specifically, how transparent it truly was, and who ultimately exercised control behind the scenes.

MACC Has Opened Three Investigation Papers

In a related development, the Malaysian Anti-Corruption Commission (MACC / SPRM) has formally opened three investigation papers involving IJM Corporation Berhad. The scope of these investigations includes overseas investments estimated at approximately RM2.5 billion, governance concerns surrounding specific projects, as well as allegations involving the use of insider information for share trading.

MACC Chief Commissioner Azam Baki has personally confirmed that the investigations also cover claims of “share tip-offs” involving both Sunway Berhad and IJM. This confirmation reinforces the seriousness of the case and underscores that the investigations into IJM and Sunway cannot be prematurely concluded—particularly in light of the allegations of bribery payments linked to Jeffrey Cheah and other parties involved.

Call: MACC Investigation Must Not Be Halted

Assertions by Jeffrey Cheah that Sunway Berhad is free from corruption, as stated in a written response, cannot be accepted at face value and should not be used as a basis to curtail ongoing investigations.

The allegations surrounding Jeffrey Cheah—alongside the involvement of major institutions such as Permodalan Nasional Berhad (PNB) and the Employees Provident Fund (EPF / KWSP), as well as a network of high-profile individuals—are of sufficient gravity to warrant a comprehensive, transparent and independent inquiry.

While the failed acquisition of IJM Corporation Berhad by Sunway may have closed one chapter, it has simultaneously opened a far larger and more consequential one: the question of who truly controls the direction of public investment funds. If the circulating allegations hold any substance, this transcends a corporate dispute and enters the realm of national interest.

The Malaysian Anti-Corruption Commission (MACC / SPRM) now stands at a critical crossroads—whether to fully uncover the truth or allow key questions to remain unresolved under the weight of influence and power. The situation raises broader concerns about accountability, particularly in light of past corruption cases linked to data centre operations, where enforcement outcomes have drawn scrutiny. Reports that individuals allegedly involved in bribery amounting to RM7.5 million, including the destruction of RM1 million in evidence, were released with only a compound settlement continue to fuel public concern over consistency in enforcement.

In a case of this magnitude, anything less than a thorough and uncompromising investigation would fall short of public expectation.